By Richard Mazzochi and Minny Siu King & Wood Mallesons’ Hong Kong office.

What does the FSDC report recommend?

What does the FSDC report recommend?

The Financial Services Development Council (“FSDC”) has just released its review of Hong Kong’s listed structured products market. The FSDC published its report on 18 April 2017. The report sets out the FSDC’s key findings following its comprehensive review of the listed structured products market, particularly in comparison to European markets.

King & Wood Mallesons, represented by Richard Mazzochi and Minny Siu, partners of KWM’s banking and finance department in Hong Kong, advised the FSDC working group on its report. “We are honoured to be invited by the FSDC to work alongside other industry members on this timely initiative by the FSDC. Hong Kong is a leading global structured products market. This review and its recommendations will assist Hong Kong maintain its position as a leading global structured products market and wealth management and investment centre in Asia.” said Richard Mazzochi and Minny Siu.

Which aspects of the current listed structured products market in Hong Kong might be improved?

Although Hong Kong’s listed structured products market has the highest turnover globally, its product range is limited to warrants and CBBCs (both of which are highly leveraged). Hong Kong’s regulatory regime supports a wide coverage of product types and underlying asset classes, but warrants and CBBCs are confined to limited types of underlying assets (namely Hong Kong stocks, Hong Kong stock indices, overseas stock indices and currency pairs and commodities).

As a result, Hong Kong investors lack access to non-leveraged listed structured products which:

- offer more transparency and liquidity;

- are already somewhat familiar to Hong Kong’s investors because unlisted products with similar features are already available and understood by investors; and

- do not require the investor to pay margin in adverse market conditions, i.e. the investor will not lose more than the amount initially invested.

What are the key recommendations proposed by the FSDC?

The report makes two key recommendations: (i) expansion of listed structured product types, and (ii) other ancillary recommendations to enhance the product issuance process and to encourage market participants to launch new listed product types. The ancillary recommendations include:

- establish a clear framework and timetable for new product approval and issuance;

- formulate a clear set of eligibility requirements for underlying assets;

- create a designated communication channel between issuers and regulators; and

- review the new product issuance process.

The report does not propose any change to the current regulatory regime. The key recommendations can be achieved under the existing regulatory framework but there is, in the FSDC’s view, room for the new product issuing process to be improved to encourage issuers to launch new products.

1. Expansion of non-leveraged listed structured product types

The report recommends introducing new categories of listed structured products currently available in European markets, starting with Discount Certificates and Bonus Certificates. Discount Certificates and Bonus Certificates are non-leveraged products that offer investors an enhanced return. An investor’s exposure to the shares underlying these products is not worse than if the investor held the shares directly. They have a pay-off mechanism similar to unlisted equity linked investments currently available to investors in Hong Kong.

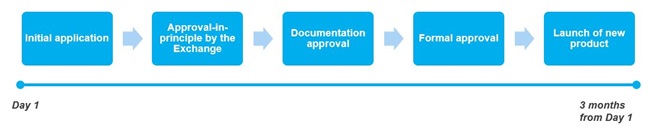

2. Enhancements to listing process with shorten “time-to-market” timeframe for new products

The report recommends implementing a clearer framework and approval timeframe for processing an application to launch a new listed structured product type. The FSDC suggests the entire process should be no longer than three months. The new product application framework should, at minimum, guide issuers through the following stages[1]:

More business opportunities for issuers in Hong Kong, and investment opportunities for retail investors

Unlisted versions of structured products with similar features to Discount Certificates and Bonus Certificates are already popular with Hong Kong investors. A recent SFC survey indicated that structured investment products accounted for 44% of the aggregate transaction amount of investment products sold[2].

The listed market offers a number of advantages over the unlisted market, including:

- standardised product terms – easier for investors to understand and compare listed structured products of the same type;

- mandatory liquidity services – investors have the benefit of an active secondary market to sustain the liquidity of the product during its term; and

- pricing transparency – pricing information relating to listed structured products is generally much more transparent.

KWM welcomes the efforts made by the FSDC to promote product innovation for retail investors. We look forward to working with market participants to bring new products to the market in the coming year!

The full report and FAQ can be downloaded from the FSDC website at www.fsdc.org.hk/en.

[1]See section 5.3(b) of the Report.

[2]According to the Survey on the Sale of Non-exchange Traded Investment Products published by the SFC on 9 December 2016, unlisted structured products in the aggregate transaction amount of HKD167 billion were sold to individual investors in the year ended 31 March 2016. The survey is available athttp://www.sfc.hk/web/EN/files/ER/PDF/Product%20Survey%20report_Mar%202016_Eng.pdf, p. 7.