In Germany, regulatory aspects can typically be handled very smoothly. Unlike some other jurisdictions, most investments in Germany do not call for substantial regulatory issues to be addressed. For example, subject only to a few exceptions and notification requirements, Germany does not generally restrict the export or import of capital.

There are, however, a few areas which do require attention, and the following issues are those we typically address in the context of Chinese investment in Germany.

Merger control

Acquisitions will require notification to, and clearance from, the German competition authority, the Federal Cartel Office, if (1) they qualify as reportable concentrations, and (2) the parties meet certain turnover thresholds.

Concentration

The German Competition Act lists several transaction scenarios which qualify as concentration. The most important scenarios are the following:

- Acquisition of control: this scenario is met where the purchaser acquires a majority of the shares or voting rights in a target company and is, therefore, able to define the operations of the target company. Minority shareholdings (below 50%) can qualify as acquisitions of control where the purchaser has veto rights in relation to key strategic business decisions of the target company;

- Acquisition of shares: this scenario is met where the acquisition results in the purchaser crossing one of the thresholds of 25% or 50% of the capital or voting rights in a target company.

Turnover thresholds

In general, concentrations will have to be notified if the parties meet the following cumulative turnover thresholds:

- The parties’ combined worldwide turnover exceeds EUR 500 million; and

- One of the parties (acquirer or target) has national turnover in Germany of more than EUR 25 million; and

- The other party (target or acquirer) has national turnover in Germany of more than EUR 5 million.

If the (higher) turnover thresholds triggering merger control clearance at the European Level are met, competent authority for merger control clearance will be the European Commission and not the Federal Cartel Office.

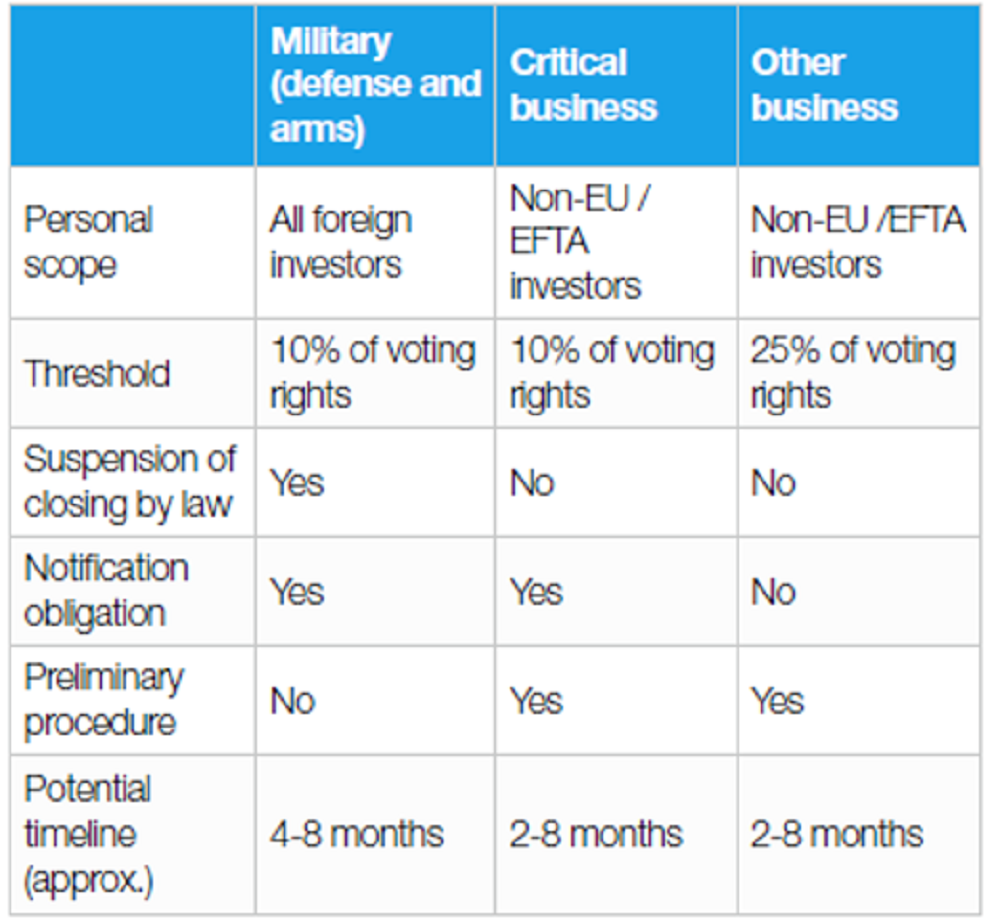

Foreign direct investments

While the German merger control rules focus solely on the competition aspects of transactions, investments in German companies by non- EU/EFTA investors such as Chinese investors can also be reviewed by the German Ministry of Economics with regard to their impact on German national public order and security.

As the total number of Chinese investments in German enterprises has grown considerably over the last years, the relevance of this foreign investment control review has evolved in parallel. The scope of relevant provisions has been extended during the last years with further changes expected to come.

The table below sets out a short overview of the key aspects of this procedure:

As most transactions concern a non-military business, the parties often initiate a preliminary procedure applying for a certificate of non-objection to achieve legal certainty, i.e. confirmation that the Ministry will not intervene. Unless the Ministry opens a full review, such confirmations can be obtained within one or two months, and this process will often be conducted in parallel to the merger control proceedings. A recent tightening of the relevant rules, has resulted in more reviews being initiated by the parties and longer review periods being available to the regulators. While this may impact the timing of a transaction, there are hardly any cases that are not approved.

Beyond Germany, the European Union has recently adopted a new regulation establishing a framework for the screening of FDI into the European Union (FDI Regulation). It is the first ever EU level tool to screen FDI on grounds of security and public order. A key development is that FDI Regulation now sets up a cooperation mechanism between member states and the European Commission, determines certain screening factors and specifies which information should be made available as part of the cooperation. Despite the additional cooperation mechanism, member states will retain the power to review foreign direct investment on national level.

In the context of many projects, specific legal expertise with regard to regulatory aspects is needed to meet the client’s needs and their global strategy, e.g. in the form of national or EU merger control advice or specific competition counsel in other jurisdictions.

In these cases, the KWM Frankfurt office works seamlessly with our offices in Brussels, Beijing or in the other jurisdictions in which we practice, as well as with experts in best-friends firms in those where we do not. We also co-operate closely with specialised law firms, investment banks, auditors and other advisors in Germany or other jurisdictions to get the client’s deal done.