By King & Wood Mallesons

What are the main features of Australia’s tax system?

Australia has a comprehensive tax regime with taxes imposed at both the Federal level and the State/Territory level. The Australian Taxation Office (ATO) is responsible for administering the tax laws imposed at the Federal level and each State and Territory has a different body which administers the tax laws imposed in that particular jurisdiction

The Australian tax regime is complex. Australian tax laws also change frequently, both in response to changes at a domestic level (such as a change in government) and changes at an international level (such as the recent OECD BEPS initiative). Given the ever changing nature of the Australian tax system, you should always consult with your Australian tax adviser before engaging in any transaction which has a connection to this jurisdiction.

We outline in further detail below:

- the core concepts relevant to the imposition of Australian income tax;

- some of the key issues that are relevant for entities investing into Australia; and

- an overview of some of the other transaction taxes imposed in Australia.

Australian income tax

Australian income tax is levied annually on the “taxable income” of an entity, which is equal to an entity’s “assessable income” less “allowable deductions”. The income year in Australia runs from 1 July to 30 June.

The assessable income of an entity is based upon its tax residency. Broadly:

- Australian residents must include in their assessable income both ordinary income (i.e. revenue gains) and statutory income (i.e. capital gains) from all sources (i.e. their worldwide income); and

- non-resident entities must include in their assessable income both ordinary income which has an Australian source and other amounts which are specifically required to be included pursuant to the tax law, such as any capital gains arising on the disposal of Australian real property interests.

Allowable deductions include general business outgoings to the extent they are incurred in gaining or producing assessable income or in carrying on a business. A number of specific deductions are also provided for in the tax law.

If a taxpayer’s allowable deductions exceed their assessable income for a particular income year, this may give rise to a tax loss for that year which may be carried forward and applied against their assessable income in a subsequent income year. However, companies and trusts must satisfy stringent statutory tests before being able to utilise tax losses in this manner.

Australia has a comprehensive set of double tax treaties (DTT) with other jurisdictions which may also be relevant to non-resident entities. The Australian tax law provides that to the extent that our tax laws are inconsistent with a DTT, the DTT will prevail. This means that if the Australian tax law seeks to impose income tax on a particular gain or amount of income but the relevant DTT allocates the taxing rights to the other jurisdiction, no Australian income tax will generally be imposed.

Certain other types of income received by a non-resident entity, such as dividends, interest and royalty payments received from an Australian entity, may also be subject to Australian income tax by way of a final withholding tax.

Residency

The tax residency of an entity is fundamental to understanding how the Australian income tax law will apply to that entity.

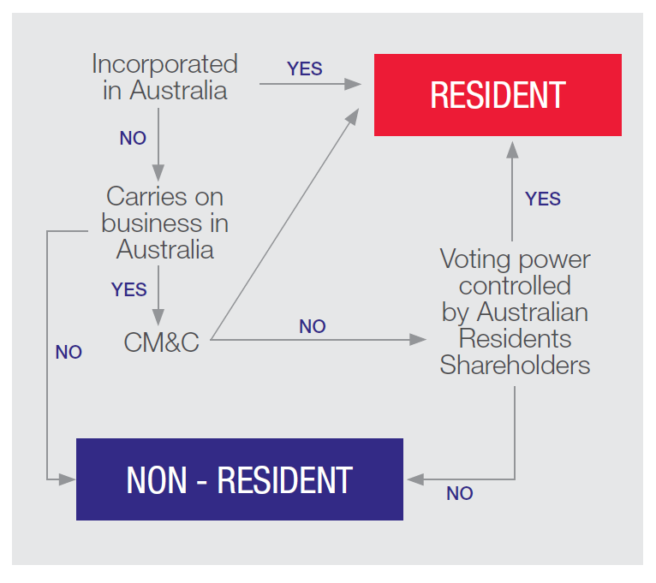

A company will be an Australian resident for income tax purposes if it is incorporated in Australia. A company that is not incorporated in Australia can still be an Australian tax resident as indicated in the diagram below:

There is no definitive test as to what constitutes central management and control (CM&C) but factors such as where board meetings are held, how day to day management occurs and where investment decisions are made will be relevant in determining where the CM&C of a company is exercised.

The residency tests for other types of entities are summarized in the table below:

Nature and source of income

Revenue vs capital

There is a significant body of case law and ATO guidance in Australia which is relevant in determining whether an amount of income or a particular gain is on “revenue account” or “capital account”.

Income or gains which are on revenue account will generally form part of a taxpayer’s ordinary income whereas income or gains which are on capital account will form part of their statutory income (as statutory income includes any net capital gains).

The revenue / capital distinction is important for the following reasons:

- different categories of tax losses can only be applied against certain categories of assessable income. Most importantly, carried forward capital losses cannot be used to offset a revenue gain in a future income year;

- the capital gains tax (CGT) provisions contain a number of concessions which do not apply to revenue income or gains. Accordingly, it may be advantageous for a gain to be on capital account because this will result in a lower income tax liability for the taxpayer after applying the relevant concession; and

- non-residents will generally not be subject to income tax in Australia on income or gains which are on capital account unless it arises in connection with the disposal of, or dealing in an Australian real property interest (which may include an interest in a company or trust which itself holds Australian real property).

In broad terms, income or gains made in the ordinary course of carrying on a business will be on revenue account. Examples would include profits from ordinary trading activities (i.e. selling products to customers).

Transactions will be taken to be on capital account where they involve the mere realisation of an asset that was either held for a long period of time or was acquired with the intention of holding it for a long period of time.

Source

The Australian tax laws do not contain comprehensive source rules so this is generally determined on the basis of common law principles. Factors such as where trading activities take place and where relevant contracts are signed may be relevant in determining whether an amount of income or a particular gain has an Australian source.

Again, foreign residents will need to consider the application of any DTT, because even if an amount of ordinary income has, prima facie, an Australian source, many DTTs will contain a provision that will not allow Australia to impose income tax on any such income unless the non-resident taxpayer had a permanent establishment in Australia (known as the “business profits article”).

CGT

Unlike other jurisdictions, there is no separate CGT regime in Australia. Instead, taxpayers must include in their assessable income for a particular income year, any net capital gains made by the taxpayer in that year. Net capital gains form part of a taxpayer’s “statutory income” and are calculated by taking the total of the capital gains arising in that year and subtracting any capital losses. If a taxpayer has more capital losses than capital gains, they will have no net capital gain for that income year and may carry forward the net capital loss to future income years.

In general terms, a capital gain or capital loss will arise in connection with a “CGT event”. There are numerous events that may occur but they may broadly be broken into “disposal” events (i.e. where an asset is disposed of by one taxpayer to another) or “creation” events (i.e. where an asset such as a legal right is created).

A taxpayer will make a capital gain in connection with a CGT event if the “capital proceeds” received in connection with the event are more than the asset’s cost base. A capital loss will arise if the capital proceeds are less than the asset’s reduced cost base.

Broadly, capital proceeds include the total of the money the taxpayer receives (or is entitled to receive) and the market value of any other property that the taxpayer receives (or is entitled to receive) with respect to the CGT event. Provisions exist which deem the amount of capital proceeds received in certain circumstances, for example, if the parties to a transaction are not acting at arm’s length, then the taxpayer may be deemed to have received the market value of the asset that is the subject of the CGT event (even though they received less) and the taxpayer must calculate their income tax liability on the basis of the deemed proceeds.

Generally the cost base or reduced cost base of an asset is what the taxpayer paid to acquire the asset (plus other amounts which go to the preservation of the asset to the extent those amounts have not already been tax deducted), which again may be altered in certain circumstances.

Discount CGT concession

Certain Australian resident taxpayers may be eligible to reduce any capital gain by the CGT discount. Eligible taxpayers include individuals, trusts and complying superannuation funds. Companies are not eligible for this concession.

Broadly, the taxpayer must have held the asset that is the subject of the event for at least 12 months before the time of the CGT event. There are several other requirements that must be satisfied.

If applicable, individuals and trusts may reduce their capital gain by 50% and complying superannuation funds may reduce their capital gain by 33.3%. The reduced capital gain is then included in the taxpayer’s statutory income for the income year.

This concession is not applicable to all CGT events.

What about non-resident entities?

A non-resident entity is only required to include a net capital gain in their assessable income for certain categories of assets, known as “taxable Australian property” (TAP). If a CGT event occurs for an asset that is not TAP, the nonresident is not required to calculate whether a net capital gain arises for them.

TAP includes:

- Australian real property (including a lease of land if the land is situated in Australia);

- mining, quarrying or prospecting rights if the minerals, petroleum or quarry materials are situated in Australia;

- indirect Australian real property interests (i.e. certain membership interests in an entity (generally requiring a 10% or greater interest in the entity which is tested at particular times) where the majority of assets of that entity comprise either of the above items), noting that this test requires you to trace through interposed entities;

- assets used at any time in carrying on a business through a permanent establishment in Australia (for example, assets used by an Australian branch of a foreign company which carries on business in Australia); and

- an option or right to acquire any of the assets mentioned above.

Current tax rates

Individuals – Australian resident

Individuals – non-resident

Companies – both resident and non-resident

The current corporate tax rate is 30%.

Certain smaller companies with a turnover of less than A$10 million have a reduced rate of 27.5%.

The reduced company tax rate of 27.5% will be progressively applied to companies with a turnover of less than A$50 million by the year ended 30 June 2019. The company tax rate will then be reduced for these companies to 25% by the year ended 30 June 2027.

Other features of the Australian income tax system

Tax consolidation

Australian tax laws permit wholly-owned corporate groups to form a “tax consolidated group” which means that all members of the group are treated as a single entity for certain income tax purposes.

Tax consolidation is very common among corporate groups in Australia and has the following effects:

- most intra-group transactions are ignored for income tax purposes (for example, any gain or loss arising on the transfer of assets between members of the group would be ignored);

- tax losses and other attributes such as franking credits of the various group members are pooled together;

- group restructuring can be streamlined because assets and shares can be moved between group entities without any formal rollover requirements; and

- compliance costs are reduced as the group lodges a single tax return for a unified accounting period and makes consolidated tax payments.

There are two types of tax consolidated groups:

- “Consolidated Groups” which comprises of a single Australian head company which wholly owns one or more Australian companies.

- “Multiple Entry Consolidated Groups” which comprise at least 2 Australian companies which themselves are directly owned by a common foreign company.

To form a tax consolidated group in either scenario, the relevant entities need to make a written election with the ATO.

Dividend imputation

Australia has a dividend imputation system. This means that certain distributions made by companies may attach tax credits (called “franking credits”) which are referable to the tax that has been paid at the company level.

The system eliminates double taxation by allowing Australian resident shareholders to claim a credit for Australian tax paid by a company on the profits from which the dividend is paid and it also allows a non-resident shareholder to receive any such dividend free from any dividend withholding taxes.

Withholding taxes

Withholding taxes may be imposed on certain dividends, interest and royalty payments that are made by an Australian entity to a non-resident entity.

The rates imposed under domestic law are:

- 30% for dividends;

- 30% for royalties; and

- 10% for interest payments.

If an applicable DTT applies, the rate applicable to any of the above type of payments may be reduced in accordance with that DTT.

Furthermore, the withholding tax that may otherwise apply to dividends will be reduced under Australian tax laws if the dividends are “franked” (i.e. the dividend has franking credits attached to it which provide a credit for tax paid at the company level) or are paid out of what is known as “conduit foreign income” (meaning that the dividends are sourced from foreign profits and which pass through an Australian company under specific circumstances).

Withholding taxes may also apply to distributions from certain trusts, known as managed investment trusts (MITs). These distributions, known as fund payments, are taxed at a concessional rate of 15% (subject to comments below). There are stringent rules for what constitutes a MIT, both in terms of how the trust is organised and held and what types of investments will qualify for this concessional tax rate on distributions. MITs are generally used for widely held investments which involve an investment in Australian real estate. A 10% withholding rate applies where a Clean Building MIT makes a fund payment to a recipient in an information exchange country. A MIT is a Clean Building MIT if it holds one or more Clean Buildings and does not derive assessable income from other types of assets (other than certain incidental assets).

From 1 July 2016, where a non-resident disposes of certain types of TAP, the purchaser will be required to withhold a non-final withholding tax at a (current) rate of 12.5% of the purchase price, and remit the amount withheld to the ATO. There are certain exemptions and exclusion which may apply which would allow a purchaser to not observe this withholding requirement.

Withholding taxes also apply to natural resource payments that are made to foreign resident entities where that payment is based wholly or partly on the value or quantity of a natural resource produced or recovered in Australia. The amount to be withheld is as advised by the ATO, as before such a payment is made, the payer must notify the Commissioner of Taxation of the proposed payment.

Transfer pricing

Australia has stringent transfer pricing rules which are designed to prevent taxpayers engaged in cross-border transactions from increasing deductions or decreasing income to reduce their Australian income tax liability. The ATO may deem the consideration receivable under an international agreement to be equal to the arm’s length consideration, allowing the Commissioner to “negate a transfer pricing benefit” in certain circumstances. The rules may apply to the provision or supply of goods and services, property, technology, and the lending of money, between either members of the same group of corporations, or alternatively other parties not dealing at arm’s length.

Anti-avoidance

The Australian tax laws (both at the Federal and the State/Territory level) contain various anti-avoidance rules which purport to cancel certain tax benefits or alter the way a tax law is applied to a particular taxpayer in certain circumstances.

The Australian tax legislation contains a number of specific anti-avoidance rules as well as a general anti-avoidance law.

Other Australian taxes

Goods and Services Tax

Transactions in Australia will generally be subject to Goods and Services Tax (GST), a broad-based tax conceptually similar to the value added taxes operating in many OECD countries. GST is currently calculated at the rate of 10% on the value of the supply of a range of goods, services, rights and other things acquired in, or in connection with, Australia.

The liability to remit GST is usually on the supplier of the GST item, in which case the supplier will, as a matter of commercial practice, gross up the purchase price to recover its GST liability from the buyer. If the buyer is carrying on an enterprise and registered (or required to be registered) for GST, in most cases it will be able to claim an input tax credit equal to the GST included in the purchase price. Accordingly, it is intended that the GST liability will flow through the supply chain to the end consumers who will ultimately bear the cost of the GST (because they cannot claim input tax credits).

Certain items, known as “GST-free” supplies and “input-taxed” supplies, are not subject to GST. GST-free supplies include certain foods, exports, health services, educational services and the supply of a going concern. Input-taxed supplies include supplies of certain residential premises and financial supplies, such as transfers of units or shares in a trust or company. Input tax credits can generally only be claimed for GST items acquired for the purposes of making GST-free supplies, rather than input-taxed supplies.

Stamp duty

Each Australian State and Territory has its own stamp duty regime applicable to a range of different transactions at varying rates.

All States and Territories levy “transfer duty” on the transfer of land or any interest in land in the State or Territory in which the land is located.

The indirect acquisition of land, on the other hand, may give rise to “landholder duty” where the acquisition:

- of itself entitles the acquirer to an interest in a landholder at or above the applicable acquisition threshold; or

- when aggregated with other interests held by the acquirer, or together with its associates, results in an aggregated interest in the landholder at or above the applicable acquisition threshold.

Broadly speaking, the acquisition thresholds in each State and Territory depend on whether the landholder is a company or trust and whether or not that entity is listed on the ASX or another recognised securities exchange. A “landholder” is any entity that holds land above a certain value, which differs across the States and Territories. In business or asset transfers, the liability to pay stamp duty (if any) depends on the assets being transferred and the jurisdiction involved.

A stamp duty surcharge may be levied where foreign persons acquire direct or indirect interests in land in New South Wales, Victoria, Queensland and South Australia. The surcharges range between 3% and 7%.

Fringe benefits tax (FBT)

This is a tax paid by employers on the value of benefits provided to employees (or their associates) in relation to their employment, such as motor vehicles, schooling, health care or loans at discounted rates of interest.

The current rate of FBT is 47% and is levied by the Federal Government.

Payroll tax

This tax is paid by employers on the value of wages paid to employees.

The different States and Territories impose payroll tax in their respective jurisdictions. The current rates of payroll tax vary between jurisdictions, but are generally around 5%.